Crypto Travel Rule Explained: FATF Requirements for VASPs

Learn how the FATF Travel Rule—FATF Recommendation 16—applies to virtual asset transfers, including VASP obligations, thresholds, and compliance requirements for 2026.

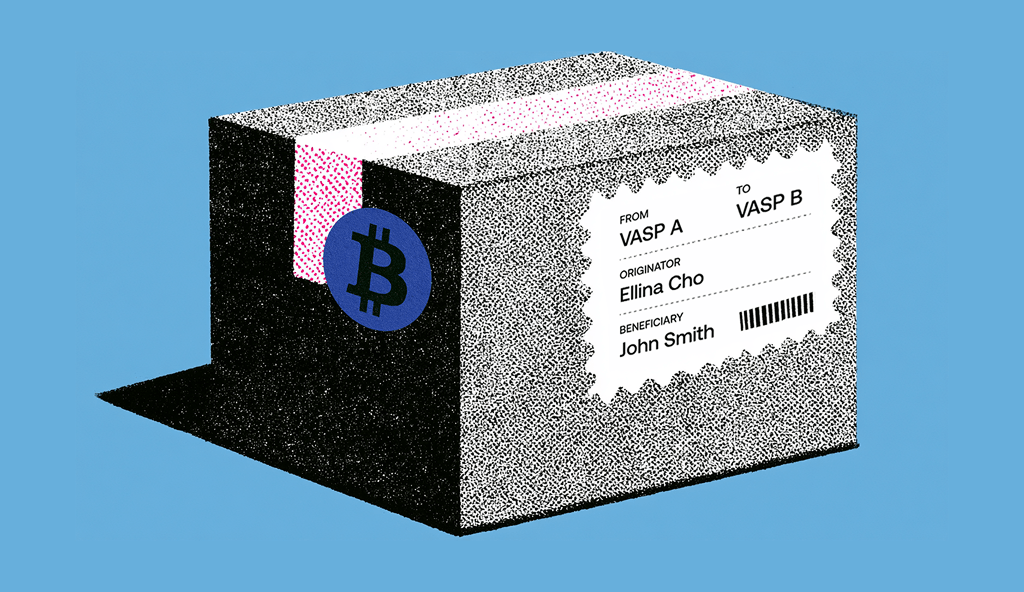

The crypto Travel Rule requires virtual asset businesses to collect, verify, and transmit information about the originator and beneficiary of virtual asset transfers.

As more jurisdictions implement the crypto Travel Rule, compliance has become a critical operational challenge for Virtual Asset Service Providers (VASPs). Businesses must determine when the rule applies, what information must accompany a transfer, how to exchange that information securely, and how to comply with different national requirements. Failing to meet these obligations can expose VASPs to regulatory action, disrupt cross-border transactions, and complicate relationships with counterparties.

This guide explains the FATF Travel Rule, the requirements that apply to VASPs, the challenges, and the jurisdictional landscape businesses need to manage in 2026.

What is the crypto Travel Rule?

The Travel Rule refers to the application of Financial Action Task Force (FATF) Recommendation 16 to virtual asset (VA) transfers. While Recommendation 16 also applies to traditional wire transfers, the term “Travel Rule” is most commonly used in the context of VA transfers.

Often referred to as the crypto Travel Rule, this requirement sets standards for transparency in crypto transfers to detect and prevent financial crime.

Under this Travel Rule framework for VAs such as cryptocurrencies, VASPs must collect information about the originator and beneficiary of a transaction, verify the information relating to their own customers, and share it with counterparties. This information must “travel” with the transfer to increase transparency and traceability.

Originally developed for wire transfers in the traditional finance sector and fiat currency, FATF Recommendation 16 has been incorporated into the national legislation of many jurisdictions and extended to cover VAs. As a result, the Travel Rule requires VASPs worldwide to implement systems that enable the exchange of required originator and beneficiary data in transactions to adapt to the evolving financial crime landscape.

Why was the Travel Rule introduced?

The Travel Rule is intended to make virtual asset transfers more traceable and help combat money laundering, terrorist financing, sanctions evasion, and other financial crimes. On-chain, these transfers are only pseudonymous—the public ledger shows wallet addresses, not identities. The Travel Rule makes the VASPs at each end attach the customer-identity information the blockchain itself doesn't carry.

As a general rule, relevant information should be provided to the appropriate regulatory authorities through suspicious transaction reporting, although this obligation falls outside the scope of the Travel Rule itself.

Who must comply with the Travel Rule?

Crypto Travel Rule obligations apply to VASPs when implemented through the national legislation of the jurisdiction in which they operate.

VASP definition and scope

A Virtual Asset Service Provider, or a VASP, is a person or business that carries out certain crypto exchange, transfer, custody, or issuance-related activities for or on behalf of another person, as a business activity.

💡Terminology varies by jurisdiction. In the European Union, businesses providing crypto-asset services are generally regulated as Crypto-Asset Service Providers (CASPs) under MiCA. In the United States, many crypto businesses fall within the definition of a Money Services Business (MSB) under the Bank Secrecy Act and FinCEN regulations, and the term VASP is not used in US legislation. Singapore regulates Digital Payment Token (DPT) service providers. Unless stated otherwise, this guide uses the FATF term VASP for consistency.

An entity is generally considered a VASP if it provides any of the following activities:

Exchange between virtual assets and fiat currencies

Exchange between one or more forms of virtual assets

Transfer of virtual assets on behalf of customers

Safekeeping or administration of virtual assets, or instruments that enable control over them

Participation in, or provision of financial services related to, an issuer’s offer or sale of a virtual asset

The Travel Rule applies to businesses in situations such as:

Virtual asset transfers involving two VASPs—the originating and beneficiary—acting on behalf of their clients. In some cases, an intermediary VASP(s) may also be involved.

Virtual asset transfers involving one—either the originating or beneficiary—VASP acting on behalf of its clients, as well as an unhosted wallet at one end.

– obtain information about the originator and beneficiary from a client who initiated a virtual asset transfer

– in accordance with the targeted financial sanctions regime, conduct AML screening against both the originator and beneficiary

– verify information about the originator by comparing it with the information gathered during the KYC or KYB

– carry out wallet attribution to establish which type of wallet—custodial or self-hosted—is used on the other end and, if it is a custodial one, establish which VASP controls the wallet

– conduct transaction monitoring and report to the FIU if a suspicious transaction is identified

– transmit information about the originator and beneficiary to the beneficiary or intermediary VASP

– keep records related to the transfer for as long as required by national legislation.

– carry out wallet attribution to establish which type of wallet—again, custodial or self-hosted—is used on the other end. If a custodial one is used, establish which VASP controls the wallet (if necessary)

– receive information about the originator and beneficiary from the originating or intermediary VASP (or obtain it directly from its customer if virtual assets are received from a self-hosted wallet) and ensure that the received information is complete by comparing it with the applicable requirements

– in accordance with the targeted financial sanctions regime, conduct AML screening against both the originator and beneficiary

– verify information about the beneficiary by comparing it with the information gathered during the KYC or KYB

– conduct transaction monitoring and report to the FIU if a suspicious transaction is identified

– keep records related to the transfer for as long as required by national legislation.

Intermediary VASP

The intermediary VASP must:

– receive information about the originator and beneficiary from the previous VASP in the transfer chain and ensure that the received information is complete by comparing it with the applicable requirements

– in accordance with the targeted financial sanctions regime, conduct AML screening against both the originator and beneficiary

– carry out wallet attribution to establish which type of wallet is used on the other end. If it is a custodial one, establish which VASP controls the wallet

– conduct transaction monitoring and report to the FIU if a suspicious transaction is identified

– transmit information about the originator and beneficiary to the beneficiary or intermediary VASP

– keep records related to the transfer for as long as required by national legislation.

In June 2025, FATF adopted revisions to Recommendation 16. The revised standard introduces more consistent data requirements, with countries expected to complete implementation by the end of 2030. This means that enforceable national rules may continue to reflect different versions of the standard during the transition.

In practice, there isn’t just one type of threshold for when the Travel Rule takes effect. Some thresholds act as “de minimis” thresholds, which set a level below which certain Travel Rule obligations may not apply, or may apply in a limited way depending on the jurisdiction.

Some thresholds also determine how much data needs to be collected and shared. In these cases, obligations apply at all transaction values, but the amount of required information increases once a transaction exceeds a certain level.

Additional thresholds may also exist. For example, some jurisdictions set thresholds for when extra checks are required, such as verifying originator and beneficiary information and verifying unhosted (self-custodial) wallets. These requirements may depend on transaction value or apply regardless of it, depending on local regulations.

The FATF’s Travel Rule de minimis threshold recommendation is USD/EUR 1,000 for VA transfers. Above this amount, it advises that the full set of identifying information must be collected and shared between obliged entities. Below the threshold, a reduced data set—the names of the originator and beneficiary, and an account number (for virtual asset transfers, typically the wallet address) or a unique transaction reference for each—still applies. This data set doesn’t need to be verified unless there is a suspicion of money laundering or terrorist financing.

However, as our jurisdictions list shows, implementation is not uniform. Individual jurisdictions determine their own limits, meaning the applicable Travel Rule de minimis threshold can vary significantly. Some countries follow the FATF’s recommended standard of USD/EUR 1,000, others set different thresholds, and some require reporting regardless of transaction value.

For example, in the United States, under the BSA regulations, a USD 3,000 de minimis threshold applies to certain transfers between financial institutions. This exceeds the FATF recommendation and shows how national rules may diverge from global guidance.

Businesses must carefully assess local regulatory requirements. Depending on the jurisdiction, information may only need to be shared above a defined limit, different data requirements may apply below the threshold, or all qualifying transactions may be subject to reporting and recordkeeping obligations.

What information must be shared under the Travel Rule?

Travel Rule crypto requirements determine what originator and beneficiary information VASPs must collect, retain, and share. The data below reflects the revised FATF Recommendation 16 standard and may be transmitted through a secure Travel Rule protocol.

Businesses must comply with the rules in force in each relevant jurisdiction, as national requirements may vary during the transition to the revised standard.

Cross-border transfer data requirements

Under the Travel Rule, the originator and beneficiary information required for a cross-border virtual asset transfer depends on the transfer's value and the threshold established by the relevant jurisdiction.

💡FATF sets the de minimis threshold at no higher than USD/EUR 1,000, with a reduced set of information applying to transfers below that threshold. Whether a transfer of exactly USD/EUR 1,000 is subject to the full information requirements therefore depends on how the jurisdiction has implemented the FATF standard.

Transfers below USD/EUR 1,000 or the applicable local threshold

Originator:

Name

Account number, or if none, a unique reference number

Beneficiary:

Name

Account number, or if none, a unique reference number

What’s changed:

No change in data scope

Transfers at or above USD/EUR 1,000 or the applicable local threshold

Originator:

Name

Account number, or if none, a unique reference number

Address (or country and town name, or nearest alternative)

For individuals: Date of birth (or year of birth where the full date is unavailable)

For legal entities, the identifiers are required 'where this exists': i.e., a connected Business Identifier Code (BIC), Legal Entity Identifier (LEI), or unique official identifier is to be included where the entity has one.

Beneficiary:

Name

Account number, or if none, a unique reference number

Country and town name (or nearest alternative)

For legal entities:

BIC, or

LEI, or

Unique official identifier

What’s changed:

Beneficiary address (country/town) is now required

Originator data is stricter:

Previously: address, ID, or place/date of birth

Now: date of birth is mandatory

Legal entity data clarified:

BIC, LEI, or official identifier required for both parties

Domestic transfer data requirements

The Travel Rule applies to both domestic and cross-border transfers, although FATF permits simplified requirements in certain domestic cases. Note, however, that FATF directs jurisdictions to treat virtual asset transfers as cross-border transfers, so the domestic regime is chiefly relevant where national law expressly applies a separate domestic regime to virtual asset transfers.

Transfers below USD/EUR 1,000 or the applicable local threshold

Originator:

Name

Account number, or if none, a unique reference number

Beneficiary:

Not required

What’s changed:

Previously unclear; now clarified

Transfers at or above USD/EUR 1,000 or the applicable local threshold

Originator:

Name

Account number, or if none, a unique reference number

Address (or country and town name, or nearest alternative)

For individuals: Date of birth

For legal entities:

BIC, or

LEI, or

Unique official identifier

Beneficiary:

Not required

What’s changed:

No major changes, except updated data requirements as above

Notes:

Countries may set a de minimis threshold

Requirements apply unless the information is already accessible to authorities or beneficiary institutions through other means

Travel Rule implementation challenges

Travel Rule AML implementation can be complex due to both regulatory and technical factors, particularly given that FATF Recommendations are highly influential but not legally binding. This means jurisdictions can choose how or whether to implement them. This largely leads to fragmented adoption and inconsistent frameworks.

Differences in transaction thresholds, privacy laws, verification standards, and implementation timelines create significant challenges for VASPs operating across multiple jurisdictions. As more countries introduce their own Travel Rule frameworks, businesses must navigate inconsistent requirements and staggered enforcement, increasing regulatory complexity.

At the same time, VASPs need processes that meet regulatory requirements and that would not disrupt the customer experience. They must also ensure data accuracy, avoid transmission failures, and maintain complete audit trails to demonstrate compliance.

Let's look at some of the most common—and most frustrating—Travel Rule challenges VASPs face today.

The "sunrise issue"—named because the sun rises at different times across time zones—describes the uneven introduction and enforcement of the Travel Rule across jurisdictions. Although Travel Rule requirements for wires and other traditional funds transfers are well established in many markets, equivalent requirements for virtual asset transfers have been introduced at different times and in different forms.

As a result, a VASP in a country with established requirements may need to exchange information with a counterparty in a jurisdiction that has not yet implemented the Rule, uses a different threshold, or cannot receive the same data fields. The originating VASP may still need to collect and retain the required information even when the foreign counterparty cannot accept it.

Firms therefore need procedures for determining whether to proceed with, hold, reject, or otherwise restrict transfers involving jurisdictions or counterparties at different stages of implementation.

Interoperability

A significant challenge in Travel Rule implementation is interoperability between Travel Rule protocols. Because VASPs may rely on different messaging standards and networks, limited interoperability can lead to failed information exchanges, delayed transfers, and compliance gaps.

The most effective way to address this challenge is to use a Travel Rule platform that supports as many widely adopted protocols as possible and provides access to a large directory of connected VASPs. Broad protocol support and a large VASP network make it easier to exchange the required information with counterparties. This reduces failed transfers and operational friction and helps businesses meet regulatory requirements across jurisdictions.

Unhosted (self-hosted) wallets

Transfers involving unhosted wallets present a significant Travel Rule challenge because jurisdictions impose different requirements on VASPs. Depending on the applicable rules and the level of ML/TF risk, a VASP may need to verify ownership or control of the self-hosted wallet, apply enhanced due diligence, or collect additional information before processing the transfer.

Counterparty identification (VASP attribution)

Accurately identifying counterparties is another headache for Travel Rule compliance. Before initiating a transfer, a VASP typically needs to determine whether the destination address belongs to another regulated VASP or to a self-hosted (unhosted) wallet—a process commonly referred to as VASP attribution. This distinction is important because the applicable Travel Rule obligations may differ depending on the type of counterparty and the requirements of the relevant jurisdiction.

Travel Rule requirements vary considerably across crypto markets. The following comparison provides an overview of the rules in seven jurisdictions. Businesses should check the applicable legislation and supervisory guidance for their particular services and transaction flows.

Jurisdiction

Threshold

Self-hosted wallet verification

Key distinction

European Union

No threshold

Ownership or control verification for qualifying transfers over EUR 1,000

Regulation (EU) 2023/1113 applies across the EU; additional due diligence is required for certain relationships with non-EU CASPs

United States

USD 3,000 for covered transmittals of funds under the BSA Travel Rule

No separate Travel Rule requirement to prove ownership of every self-hosted wallet

The US framework applies through BSA rules governing covered financial institutions and money transmitters rather than a standalone VASP Travel Rule

United Kingdom

No threshold

Risk-based; firms may request further information or establish wallet control in higher-risk cases

There are different rules for domestic and cross-border transfers

Switzerland

No threshold

Supervised institutions must verify their customer’s control over an unhosted wallet

FINMA generally permits transfers involving unhosted wallets only where the wallet belongs to the institution’s own customer and control can be established

United Arab Emirates

No threshold

No single federal requirement to verify every self-hosted wallet

Requirements differ in some respects among the federal regime, VARA-regulated Dubai, ADGM, and the DIFC

Singapore

Basic information requirements apply to DPT transfers at all values; additional information is required above SGD 1,500

Controls apply to transfers involving unhosted wallets

MAS Notice PSN02 establishes separate information requirements for transfers at or below SGD 1,500 and those above it

Canada

CAD 1,000

No general Travel Rule-specific wallet ownership verification requirement

Financial entities and MSBs must include the required originator and beneficiary information when sending covered virtual currency transfers and take reasonable measures to obtain missing information

Check each jurisdiction in more detail below.

Jurisdictions list

TR Requirements by Country

Country code

Country name

Country status

Country regulation

Country details

AR

Argentina

Not in force

Argentina's Travel Rule regulations

Ley N° 25.246 and

Resolución 49/2024 establishes that the obligated subjects must comply with the identification of the originator and the beneficiary of the transactions covered by the Travel Rule, in the terms established by the International Standards of the FATF and in the modality that the FIU establishes for the exchange and validation of said information. Information will be updated when FIU publishes clarifications.

Visit Sumsub docs for more details on the Travel Requirements by country.

AU

Australia

In force

Australia’s updated Travel Rule requirements apply to non-incidental domestic and international virtual asset transfers under the amended Anti-Money Laundering and Counter-Terrorism Financing Act and Rules. The obligations for virtual asset transfers commenced on 1 July 2026. There is no threshold, meaning the Travel Rule applies irrespective of the transfer value.

Self-hosted wallet verification is required in specified circumstances.

VASP Due Diligence must be conducted to determine whether the counterparty is a custodial VASP or a self-hosted wallet.

Visit Sumsub docs for more details on the Travel Requirements by country.

There is no requirement for self-hosted wallet verification.

VASP Due Diligence must be conducted when establishing a correspondent relationship with a VASP registered outside Bermuda.

Visit Sumsub docs for more details on the Travel Requirements by country.

BR

Brazil

Not in force

Brazil’s Travel Rule framework is not yet in force. Its implementation is divided into two phases: the first, requiring data transmission between Brazilian VASPs, must be completed by February 2, 2027; the second, covering transfers between Brazilian and non-Brazilian VASPs, must be completed by February 2, 2028, under Resolução BCB n° 520 de 10/11/2025, Circular n° 3.978 de 23/1/2020, and Lei nº 14.478 de 21 de dezembro de 2022.

Until these phases are completed, VASPs may rely on self-declarations to clearly identify the client or user, the beneficiary, the virtual asset, the amount, and the purpose of the transfer. Such self-declarations should be documented and made available to the Central Bank of Brazil in an electronic format. It is not known whether there will be a threshold.

Visit Sumsub docs for more details on the Travel Requirements by country.

Self-hosted wallet verification is required for transactions exceeding EUR 1,000, as well as if there is suspicion of money laundering or terrorist financing involving a transfer to a self-hosted digital wallet.

VASP Due Diligence must be conducted.

Visit Sumsub docs for more details on the Travel Requirements by country.

Self-hosted wallet verification is required for transactions exceeding EUR 1,000.

VASP Due Diligence must be conducted when establishing a correspondent relationship with a CASP registered outside the EU.

Visit Sumsub docs for more details on the Travel Requirements by country.

OM

Oman

In force

In force since 6 June 2023 under

Decision No. (E/35/2023), which mandates AML/CFT compliance for Virtual Asset Service Providers. There is no transaction threshold.

Self-hosted wallet verification is required for transactions exceeding EUR 1,000.

There is no requirement for VASP Due Diligence.

Visit Sumsub docs for more details on the Travel Requirements by country.

PE

Peru

Not in force

Peru’s Travel Rule framework is not yet in force and is scheduled to take effect on August 1, 2026, under updated AML regulations covering virtual asset service providers.

There will be no threshold, meaning the Travel Rule will apply to all virtual asset transfers irrespective of value.

Visit Sumsub docs for more details on the Travel Requirements by country.

PH

Philippines

In force

In force since 5 February 2021 under

BSP Circular No. 1108 and

Memorandum No. M-2023-042, with no transaction threshold.Self-hosted wallet verification is required for all transactions.VASP Due Diligence must be conducted.

Visit Sumsub docs for more details on the Travel Requirements by country.

Visit Sumsub docs for more details on the Travel Requirements by country.Find out more about Switzerland crypto regulations.

TW

Taiwan

Not in force

Not yet in force under the Money Laundering Control Act, Regulations Governing Anti-Money Laundering and Countering the Financing of Terrorism for Enterprises Handling Virtual Currency Platform or Transaction, and pending finalization of the AML Regulations for Virtual Currency Platforms.

There is no requirement for self-hosted wallet verification.

VASP Due Diligence must be conducted.

Visit Sumsub docs for more details on the Travel Requirements by country.

There is no requirement for self-hosted wallet verification.

However, for crypto asset transfers to or from a wallet address that is not registered with any CASP, the CASP must obtain from the customer, who is a party to the respective transaction, a declaration containing at least one of the following identifying details about the owner of the self-hosted wallet: full legal name; address; place and date of birth; customer number; national identification number; citizenship number; or tax identification number.

VASP Due Diligence must be conducted when establishing a correspondent relationship with a CASP registered outside of Türkiye.

Visit Sumsub docs for more details on the Travel Requirements by country.[r]

There is no requirement for self-hosted wallet verification.

VASP Due Diligence must be conducted if the total value of crypto tokens transferred is USD 1,000 or more.

Visit Sumsub docs for more details on the Travel Requirements by country.

GB

UK

In force

In force since 1 September 2023 under the

The Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017, and the

JMLSG Guidance, with no transaction threshold.Self-hosted wallet verification is required depending on the risk level. Where a VASP has determined that information should be requested, it should take reasonable steps to obtain the information from its own customer. In higher risk cases, firms should consider taking further steps to ascertain the source of funds in the unhosted wallet and thereafter consider authorising the transfer only if the control over the unhosted wallet can be reasonably established through appropriate solutions (e.g. micro deposit or cryptographic signature).

There is no requirement for VASP Due Diligence.

Visit Sumsub docs for more details on the Travel Requirements by country.Find out more about UK crypto regulations.

There is no requirement for self-hosted wallet verification.

There is no requirement for VASP Due Diligence.

Visit Sumsub docs for more details on the Travel Requirements by country.

What happens if a VASP doesn’t comply with the Travel Rule?

Travel Rule violations are investigated and enforced by the national regulators and competent authorities responsible for implementing AML/CFT laws in their respective jurisdictions.

Depending on the jurisdiction and seriousness of the breach, consequences may include:

Directions to correct deficient policies, systems, or records

Remediation programs

Increased supervisory scrutiny

Administrative or financial penalties

Restrictions on particular services

Suspension, restriction, or withdrawal of a VASP’s license or registration

Civil or criminal consequences where provided for by national law

Liability for directors or senior management

Loss of banking, correspondent, or VASP counterparty relationships

Criminal prosecutions specifically for Travel Rule non-compliance remain rare. Most enforcement to date has taken the form of fines, remediation orders, and license restrictions rather than prison sentences. But that track record reflects the rule's relative youth (FATF only extended it to virtual assets in 2019) more than any leniency built into the framework. The civil and criminal provisions exist precisely so regulators have escalation options as enforcement matures, and traditional finance's Travel Rule, which has been in force since 1996, shows where crypto enforcement is likely headed: FinCEN has referred aggravated BSA recordkeeping failures for criminal prosecution for decades. Non-compliant VASPs that treat the criminal liability line as theoretical are betting against a rule that hasn't finished ramping up yet.

VASP Travel Rule compliance checklist

The following checklist is based on guiding questions developed in FATF discussions to support the implementation and interoperability of Travel Rule solutions. It is not exhaustive but highlights key considerations for VASPs.

🔗 Interoperability with other Travel Rule solutions

☐ Is the tool or solution interoperable with other Travel Rule tools?

☐ What type of interoperability is built into the solution?

☐ Has interoperability testing been conducted (e.g., pilot, functional, stress, or live data testing)?

☐ What was the scope of testing (e.g., data types, participating VASPs)?

☐ Are there plans for future interoperability testing or expansion?

⏱️ Timing and scope of Travel Rule data submission

☐ Can the solution support Travel Rule data submission for transfers below USD/EUR 1,000 to meet varying jurisdictional thresholds?

☐ Does the solution cover all relevant virtual asset (VA) types?

☐ Can it securely handle high volumes of transactions across multiple jurisdictions?

☐ Does it allow flexibility in data sharing (e.g., restricting data transmission to certain jurisdictions due to sanctions or risk concerns)?

📊 Recordkeeping and Transaction Monitoring

☐ Does the solution support compliant recordkeeping (e.g., retaining data for at least 5 years)?

☐ Can VASPs easily access and download stored data when required?

☐ Does the tool facilitate effective transaction monitoring and auditability?

Join our Travel Rule directory for easy compliance

Avoid costly multiple vendors with one full-cycle verification solution that includes Travel Rule, anti-fraud, KYC, and Crypto Transaction Monitoring tools.

The crypto Travel Rule is the application of FATF’s payment-transparency requirements to transfers involving virtual assets. It requires VASPs to obtain, verify, and transmit to another VASP in the transfer chain information about the originator and beneficiary of a virtual asset transfer.

What does the FATF Travel Rule require?

The FATF Travel Rule requires VASPs to obtain, verify, and transmit information about the originator and beneficiary of virtual asset transfers.

Does the Travel Rule apply to all VASPs?

No. Being classified as a VASP does not mean that every activity or transaction carried out by the business is automatically subject to the Travel Rule. Whether the Travel Rule applies depends on the specific service being provided, the nature of the transaction, the parties involved, the applicable jurisdiction, any relevant value thresholds, and how the jurisdiction has implemented the relevant legal requirements.

In practice, many VASPs offer multiple virtual asset services, some of which involve virtual asset transfers while others do not. The Travel Rule generally applies when a VASP acts as the originating or beneficiary institution in a virtual asset transfer on behalf of a customer, rather than simply because the entity is classified as a VASP. Other AML/CFT obligations may continue to apply even where the Travel Rule itself does not.

What is the BSA Travel Rule vs FATF Travel Rule?

The BSA Travel Rule and the FATF Travel Rule share the same objective—improving transparency in financial transactions to combat money laundering, terrorist financing, and other financial crimes—but they have different origins and legal status.

The BSA Travel Rule is a US legal requirement established under the Bank Secrecy Act. It was introduced by the US Treasury in 1996 and required financial institutions to transmit certain originator and beneficiary information with qualifying funds transfers.

The FATF Travel Rule, by contrast, is an international standard based on FATF Recommendation 16. This Recommendation has long applied to wire transfers, and in 2019 the FATF updated its standards to extend Travel Rule requirements to virtual asset transfers conducted by VASPs. FATF recommendations are not legally binding themselves—jurisdictions implement them through their own national laws and regulations.

Although the two frameworks differ in origin and legal authority, they pursue the same goal of increasing transaction transparency and supporting the detection and prevention of financial crime.

How do VASPs comply with the Travel Rule?

VASPs comply by identifying the applicable jurisdictional rules, collecting and verifying required information, identifying counterparties, and transmitting the necessary data through compatible Travel Rule protocols.

Not everyone loves compliance—but we do. Sumsub helps businesses verify users, prevent fraud, and meet regulatory requirements anywhere in the world, without compromises. From neobanks to mobility apps, we make sure honest users get in, and bad actors stay out.