Banks and neobanks

Handle compliant onboarding at scale with real-time AML and fraud monitoring. Keep audit-ready logs across products and regions. Resolve identity across accounts and channels.

Learn more

Orchestrate identity verification checks, code-free. Place checks at any stage of the customer journey for top anti-fraud protection and pass rates worldwide.

Handle compliant onboarding at scale with real-time AML and fraud monitoring. Keep audit-ready logs across products and regions. Resolve identity across accounts and channels.

Learn moreVerify merchants and agents automatically with KYB checks. Monitor transactions across terminals and channels. Reduce chargeback and payment fraud.

Learn moreScore P2P and cross border risk in real time. Detect mules and account takeover with device and network signals. Stay compliant with Travel Rule and sanctions checks while onboarding genuine users fast.

Verify thin-file customers with alternative signals. Catch synthetic IDs and loan stacking. Score repeat borrowers based on behavior. Run fraud and AML controls that work with credit workflows.

Need the Ideal Solution?

Optimize your fraud detection and response strategy, where cost reduction is achieved effortlessly. Avoid internal development expenses with easy configuration and pre-designed anti-fraud rules.

73

Net Promoter Score

92%

Ease of use

90%

Ease of setup

* According to G2 2025 Identity Verification Spring Report

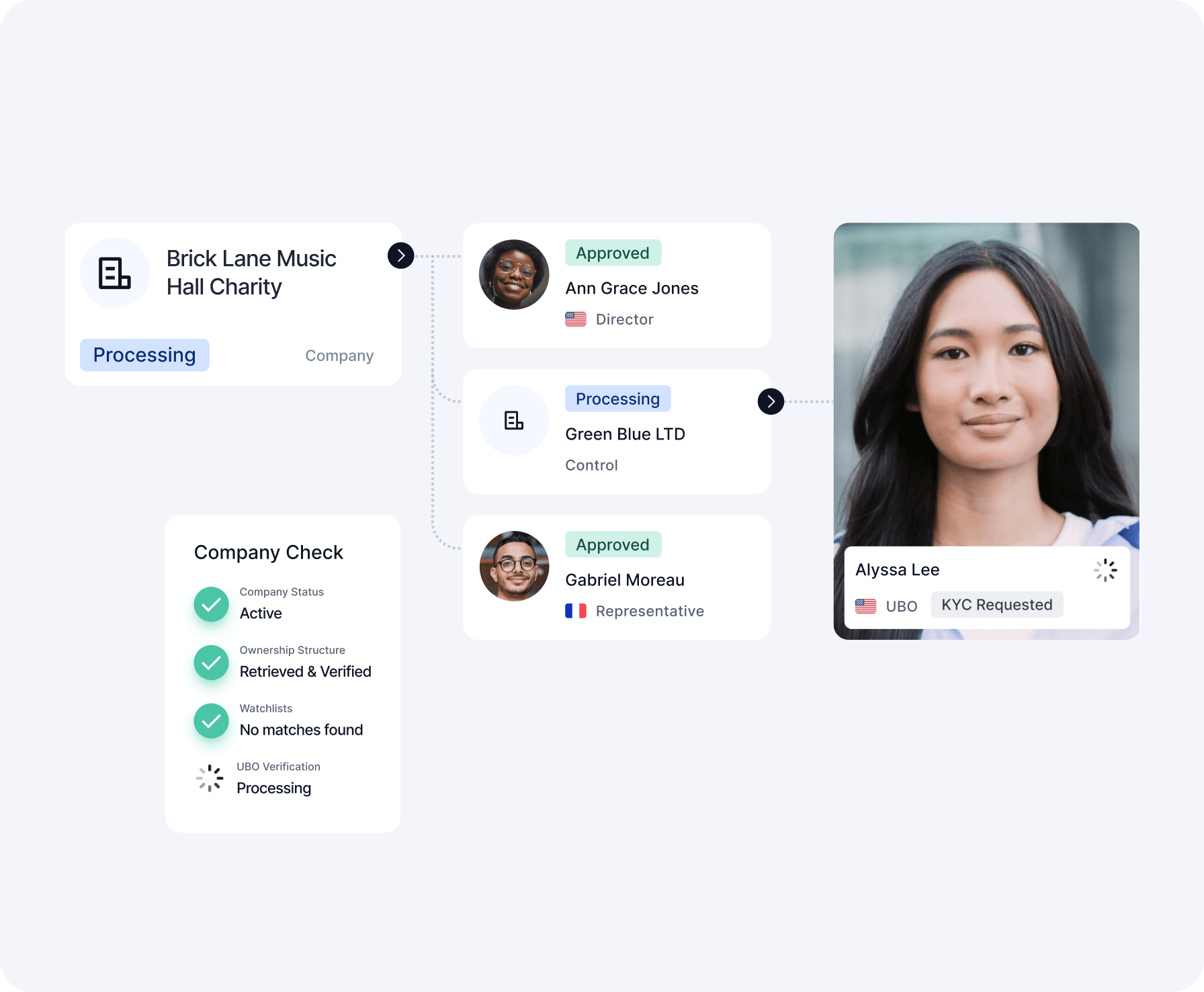

KYC/AML for financial services is often mandatory, as such businesses likely face risks associated with illicit funds and transactions. Financial service identity verification allows banks, platforms, and applications to combat money laundering, terrorism financing, and other criminal activities.

Financial institutions use online identity verification (financial service KYC solutions). In most cases, such solutions perform financial serviceidentity verification that validates customers’ government-issued IDs, such as passports or driver's licenses. Besides that, companies may verify other document types (for example, proof of address) or customer live presence (liveness checks).

KYC (Know Your Customer) is a process used by financial institutions and financial service companies to verify the identity of their customers and assess potential risks of fraud or money laundering. A financial service KYC solution is a set of tools and procedures that enables financial service companies to comply with regulatory requirements and perform efficient and accurate customer due diligence.

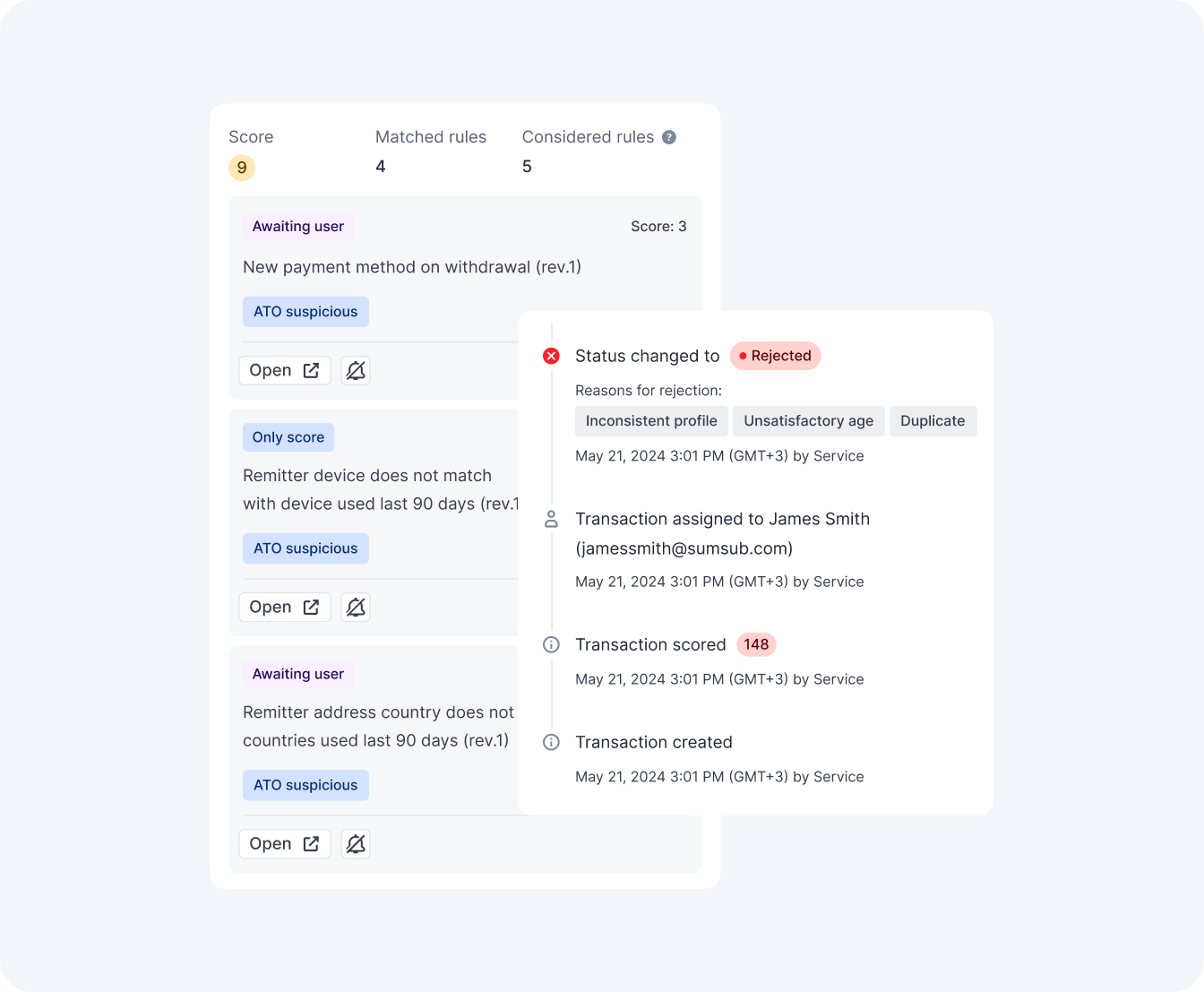

Transaction monitoring in financial services is an ongoing process that helps companies detect suspicious user activity. It monitors transactions in accordance with specified parameters and identifies unusual patterns in money transfers. This process allows financial services companies to detect fraud and report it to authorities.

Financial services identity verification is the process used by financial companies to confirm the identity of their clients. It typically involves verifying personal details like name, address, and date of birth against government-issued IDs. Advanced methods may include biometrics, facial recognition, or government database checks.

Fraud prevention in finance is how banks and financial companies try to intercept scams and stop criminals from stealing money. Fraud Prevention software that watches for suspicious activity like weird transactions or someone trying to log into your account from another country. It covers stolen credit cards, fake identities, and all other types of account fraud.