- Mar 06, 2026

- 10 min read

The Three Stages of Money Laundering: How Placement, Layering, and Integration Work in 2026

The three stages of money laundering revealed: placement, layering, and integration. Understand how each stage works and how businesses detect and prevent it.

The global scale of money laundering is vast. According to the United Nations Office on Drugs and Crime (UNODC), between 2 and 5% of global GDP is laundered each year, which amounts to between $754 billion and $2 trillion.

In most jurisdictions, ML is a serious crime punishable by imprisonment and/or significant fines. For example, in the USA, the penalty for involvement in money laundering can reach $500,000 or twice the value of the property involved in the offense, whichever is greater, and maximum imprisonment of up to 20 years, or both.

Failing to prevent money laundering can also be very serious, especially for businesses with regulatory Anti-Money Laundering (AML) obligations, such as financial institutions. Barclays Bank was fined £42 million (~USD57 million) in 2025 for AML failings, while TD Bank was hit with a historic penalty of $3 billion in 2024. This shows the scale of the risk businesses take if they do not get on top of their Anti-Money Laundering obligations.

Understanding the processes involved in money laundering is really important. Traditionally, this has been broken down into three key stages - placement, layering, and integration; however, it’s not always quite so simple.

Let’s explore what ML is, how the stages have evolved, common money laundering schemes, and how it can be prevented.

What is money laundering?

Money laundering is the process of concealing the origin of money obtained from illicit activities, like drug trafficking, bribery, or fraud. The purpose of money laundering is to introduce illicit funds into the financial system under the guise of ‘clean’ money, so that criminals can use it without attracting undesirable attention from authorities.

Money laundering can occur even when a company’s employees are unaware that the activity is taking place or do not understand what money laundering is. Although the financial services industry has traditionally been considered the most susceptible to money laundering and was once the primary target for criminals, criminal networks now use a wide range of industries to launder illicit funds.

Arina Rumiantseva

Legal Counsel, KYC Legal Lead at Sumsub

Money laundering, terrorism financing, and proliferation financing

The fight against money laundering, terrorism financing, and proliferation financing is closely connected because all three involve the movement and misuse of funds within financial systems.

AML (Anti-Money Laundering) focuses on preventing criminals from disguising the origins of illicit funds.

CTF (Countering the Financing of Terrorism) targets financial flows used to support terrorist activities.

CPF (Countering Proliferation Financing) addresses the funding of activities related to the proliferation of weapons of mass destruction.

Because these risks often overlap in financial transactions, regulatory frameworks typically address them together under the broader AML/CTF/CPF compliance regime.

The growth of money laundering

Money laundering activity has increased significantly in recent years. According to a Eurojust report, cases have risen sharply since 2016 and are expected to continue growing, posing increasing risks to businesses and financial systems.

This trend is reflected in the growing number of Suspicious Activity Reports (SARs) filed by financial institutions. Data from the US Financial Crimes Enforcement Network (FinCEN) shows a steady rise in reporting:

- 2022: ~4.3 million SARs filed

- 2023: ~4.6 million SARs filed (the highest number on record)

- 2024: ~4.7 million SARs filed, roughly 12,870 reports per day

Overall, SAR filings have increased year-on-year, indicating heightened reporting activity and a growing focus on detecting suspicious financial behavior.

A similar pattern can be observed in Europe. For example, reports submitted to the Luxembourg Financial Intelligence Unit (FIU) rose significantly:

- 2023: 44,296 suspicious transaction reports

- 2024: 50,900 reports

Beyond reporting statistics, global estimates highlight the enormous scale of the problem. International estimates suggest that $1–1.6 trillion in illicit financial flows leave developing and transition economies annually, often linked to corruption, tax evasion, and other criminal activity. Because proceeds of corruption frequently need to be laundered before entering the financial system, there is a strong connection between money laundering and corruption. Strengthening AML measures can therefore play an important role in reducing corruption and supporting economic development.

Before examining how financial institutions combat these risks, it is important to understand how money laundering works and the stages it typically involves.

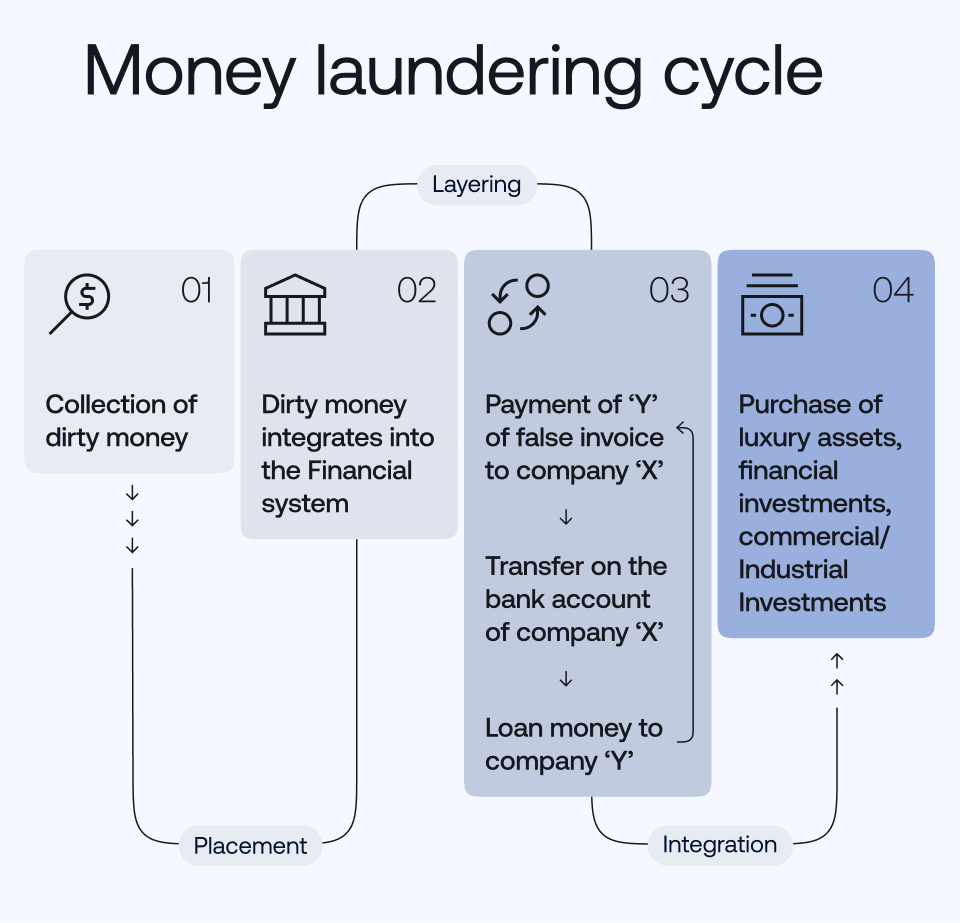

The 3 stages of money laundering

Traditionally, the money laundering process has been explained using the ‘three stages of money laundering’ model. These stages are:

- Placement

- Layering

- Integration/extraction

💡However, modern financial crime rarely follows such a clear sequence of money laundering stages. Today, money laundering is increasingly viewed as a multi-layered, multi-stage process where steps overlap, repeat, or occur simultaneously across different systems and jurisdictions.

That said, looking at the traditional three stages of money laundering does provide a good grounding in some of the key processes used by criminals.

Stage 1: Placement

In money laundering, the placement of illegal funds into the financial system may occur either directly or indirectly. Direct placement typically involves cash, while indirect placement may occur through intermediaries, businesses, casinos, or other channels.

The most popular method used in the placement stage is to divide large amounts of cash into less suspicious smaller sums (structuring), which can then be deposited into a single bank account or several bank accounts (which could involve the ‘smurfing’ money laundering technique).

Suggested read: What is smurfing?

Other methods of placement in money laundering include:

- False invoicing (over-invoicing and pseudo-invoicing for payment of non-existing goods or services)

- Blending illegal money with legitimate money

- Buying foreign currency

- Buying securities or insurance with cash

- Gambling and betting on sports events

- Using Shell companies to falsify business activity

- Loan-back schemes

- Real Estate deposits

Stage 2: Layering

“Layering” is the process of separating illicit money from its source and creating “layers” of transactions to confuse an audit. The purpose of layering in money laundering is to hide the origins of illegally obtained assets. This stage is considered to be the most complex, as it involves multiple transactions, often including international money transfers.

For the purposes of money laundering layering, money can be moved through the purchase and sales of investments, or through a series of accounts at banks in different countries. Most often, such funds are directed to jurisdictions that have loose AML regulations or do not cooperate with AML investigations.

The most “popular” examples of the layering in money laundering include:

- Investing in real estate

- Reselling high-value goods

- Transferring funds between countries

- Chain-hopping (converting one cryptocurrency to another, and moving crypto from one blockchain to another)

- Gambling Cycling

Due to the complexity of layering, AML processes must be highly sophisticated if they are to spot and prevent this type of activity.

Placement vs layering: Key differences

Placement, layering, and integration are all separate parts of the money laundering lifecycle, but when it comes to placement vs layering, there is often some confusion about how they are different.

While placement injects illicit funds into the financial system, layering hides the source of these funds through a series of transactions and financial tricks.

Stage 3: Integration

After placement and layering, integration is the next step. Criminals integrate—or, in other words, “return”—illicit money to themselves in a way that appears “clean.” If the money laundering integration stage is successful, the funds are now part of the legitimate financial system and can be used freely.

The main objective of integration in money laundering is to launder the money without attracting law enforcement attention. This can be done, for instance, by purchasing property, art, jewelry, or luxury automobiles.

Common money laundering schemes (2026)

Criminals use all available financial instruments—from NFTs to real estate—to make their illicit funds look legitimate through various money laundering schemes.

Money mules

Money mules are individuals recruited by criminals to move or transfer illicit funds on their behalf. Because money mules often have legitimate bank accounts and a clean financial history, their transactions may initially appear less suspicious, making it easier for criminals to move stolen or illegal money through the financial system.

Money mule scams are commonly used to recruit participants. Criminals often approach potential recruits through online job postings, social media, messaging apps, or dating platforms, promising easy money or remote “financial agent” work. In some cases, individuals may not realize they are participating in illegal activity.

In a typical money muling scheme, the mule receives funds into their bank account—often from fraud, phishing, or other criminal activity—and is instructed to transfer the money onward, withdraw it in cash, or convert it into cryptocurrency before sending it to other accounts controlled by the criminals. By routing funds through multiple money mules, criminals attempt to obscure the origin of the money and make it more difficult for authorities to trace the laundering chain.

Suggested read: What Is a Money Mule? Red Flags, Examples, and Prevention

Money laundering through gambling, gaming, and betting

Gambling, gaming, and betting (both online and offline) are often used to launder illicit cash. Money laundering in casinos is, perhaps, the best known, but money laundering in gambling can take many forms.

Examples of money laundering here include:

- Criminals may use low-outcome bets to deposit illicit funds and later withdraw them as “winnings.” The money enters the casino or betting platform, sometimes in cash, and is then used for repeated bets with minimal losses. The remaining funds are subsequently withdrawn, allowing the player to present the money as gambling winnings—an official and potentially taxable source of funds (SoF), which is the ultimate goal.

- Money obtained from illegal sources is used to sponsor betting as a leisure activity.

- Criminals directly invest in or acquire betting shops.

A typical gambling laundering scheme may look like this:

- Placement: Illicit funds are deposited into a gambling platform or casino, sometimes in cash or through prepaid cards, payment services, or cryptocurrency.

- Layering: The criminal places multiple bets or purchases casino chips and participates in low-risk or coordinated betting activity to circulate the funds while minimizing losses.

- Integration: The remaining balance is withdrawn as gambling winnings, which can be presented as a legitimate and potentially taxable source of funds (SoF).

For operators, gambling AML processes must be robust to prevent such criminal activity.

Suggested read: The 6 Most Popular Forms of Money Laundering in Casinos

Money laundering through sports

Money laundering in sports is a serious issue. There are many ways to make—and therefore launder—money through sports: from sports betting to sponsorships to action figures. The higher the profit from these activities, the higher the risk of money laundering.

The most vulnerable sports include football (soccer), cricket, rugby, horse racing, motor racing, ice hockey, volleyball, and basketball.

Given, the sport generates over $30 billion a year, money laundering in football is a particular cause for concern.

Here is how criminals use football to clean dirty money:

- Purchase and sale of football clubs

- Player trades

- Involving football agents in ML schemes

- Sale of player image rights

- Forgery of ticket sales

Money laundering through real estate

Real estate is a high-risk sector for money laundering. One estimate suggests that as much as £10 billion ($13.3 billion) is laundered each year through the UK property market alone.

Examples of real estate money laundering techniques include:

- Using cash or complex financing schemes to purchase property

- Purchasing property through opaque companies and trusts

- Buying properties for more than they are worth

- Using “flipping” to rapidly inflate prices by buying and selling the same property multiple times

A typical real estate laundering scheme may look like this:

- Placement: Using cash or complex financing structures (e.g., trusts, shell companies, or back-loans) to purchase property.

- Layering: Transferring ownership through multiple entities or repeatedly buying and selling the property (“property flipping”) to obscure the origin of the funds.

- Integration: Selling the property and receiving the proceeds as seemingly legitimate income from a real estate transaction.

Money laundering through cryptocurrency and digital assets

Billions of dollars are thought to have been laundered through cryptocurrency in recent years, making crypto money laundering a major concern for regulators and crypto businesses. Other digital assets, such as NFTs, have also been used by money launderers.

Digital asset and cryptocurrency money laundering can take forms such as:

- Chain hopping, where criminals rapidly transfer digital assets across multiple blockchains or between different digital assets to obscure their origins

- Crypto mixers/tumblers, where illegal assets are mixed with legitimate ones, then redistributed in a way that hides the link between the original deposit and the withdrawal

- Splitting assets across multiple wallets in ever-smaller amounts to create highly fragmented transaction data that is hard to trace

- Using DeFIs

- OTC Broker Laundering

A typical cryptocurrency laundering scheme may look like this:

- Placement: Illicit funds (for example, from scams, ransomware, or fraud) are converted into cryptocurrency through exchanges, peer-to-peer platforms, or crypto ATMs.

- Layering: The funds are moved through multiple wallets, chain-hopped between cryptocurrencies, sent through mixers, or routed through DeFi protocols to obscure the transaction trail.

- Integration: The laundered assets are converted back into fiat currency through exchanges, OTC brokers, or crypto-friendly businesses, appearing as legitimate investment or trading profits.

Suggested read: 8 Crypto Scams to Be Aware of in 2025: A Guide for Businesses and Users

The impact of money laundering on business

Here are only a few of the negative consequences of money laundering for businesses:

- Reputational harm

- Money laundering penalties, such as multimillion-dollar fines or license suspension by regulators

Moreover, the impact of money laundering can be far-reaching, with damaging socio-economic effects worldwide, including:

- Fueling corruption

- Increasing crime

- Undermining the trust of foreign investors

- Widening the gap between the rich and the poor

- Slowing economic growth

For these reasons, businesses and regulators must actively combat money laundering to protect financial systems, maintain market integrity, and prevent the broader economic and social harm caused by illicit financial activity.

Regulatory fines for money laundering: Case studies

If businesses don’t monitor transactions, they risk money laundering, fraud, and other crimes occurring on their platforms. That’s why governments have been tightening their AML regulations.

Barclays Bank fined £42 million for inadequate money laundering risk management

In 2025, Barclays Bank was fined £42 million (~USD56 million) across two of its subsidiaries.

Barclays Bank UK PLC was fined £3.1 million (~USD4.1 million) and agreed to pay £6.3 million (~USD8.4 million) to clients of its customer WealthTek for whom the bank had opened a client money account. The penalty was imposed after the UK regulator, the Financial Conduct Authority (FCA), determined that the bank had failed to gather sufficient information about the money laundering risk associated with WealthTek before allowing it to open the account.

Separately, Barclays Bank PLC was fined £39.3 million (~USD52.4 million) for similar failings in its initial money laundering risk assessment of client Stunt & Co, as well as for not properly carrying out ongoing monitoring of the client.

TD Bank hit with a historic $3 billion money laundering penalty

Canada’s TD Bank was fined $3 billion in 2024 for failing to prevent criminals from transferring hundreds of millions of dollars in illegal funds through its systems. The bank pleaded guilty to conspiracy to commit money laundering and failing to take action when staff flagged highly suspicious activity, such as a customer making daily cash deposits of $1 million.

Danske Bank fined €1.82 million for negligent monitoring and maintenance of AML processes

In 2022, Danske Bank was fined €1.82 million (~USD1.82 million) by the Central Bank of Ireland. Danske Bank’s failures were linked to out-of-date data filters within its automated transaction monitoring systems, resulting in 348,321 transactions being processed without adequate AML and counter-terrorist financing (CTF) monitoring between 2015 and 2019.

Danske Bank’s money laundering troubles did not end there, however, with the bank later agreeing to forfeit $2 billion to US authorities. This was to resolve a US investigation into allegations that Danske Bank had defrauded US banks by allowing high-risk customers of Danske Bank Estonia to access the US financial system. Additionally, Danske Bank was fined 3.5 billion kroner (~USD360 million) by the Danish financial regulator.

How to detect and prevent money laundering

To keep businesses safe and aid money laundering detection, a thorough Anti-Money Laundering (AML) compliance program must be in place. It should define how the company detects, assesses, and reports financial crime, including the following measures:

- Customer Due Diligence (CDD)

- Enhanced Due Diligence (EDD)

- Ongoing Due Diligence (ODD)

- Transaction Monitoring

- Independent AML audits

Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD)

Before a customer is allowed to use a service, they must go through a Customer Due Diligence (CDD) check. This involves obtaining the customer’s information to verify their identity and evaluate whether they are involved in any crime.

In cases of higher money laundering risk, companies apply what is known as Enhanced Due Diligence (EDD) (also sometimes called ‘Enhanced Customer Due Diligence’).

Ongoing Due Diligence (ODD)

This is an extra layer of risk management that involves ongoing due diligence checks on customers and transaction monitoring.

Transaction monitoring and AML audits

Transaction monitoringin AML is used to detect suspicious activity within customer transactions. Reliable AML Transaction Monitoring software spots unusual patterns and reviews dubious transfers and transactions made in digital or fiat currencies.

Independent AML audits allow businesses to detect deficiencies and failures in their AML strategies and correct any problems before regulatory inspections to prevent fines.

Maintaining these processes effectively is key to money laundering prevention. This will protect your business from criminals while keeping regulators away.

How smurfing detection works

‘Smurfing’ or structuring works by moving a pot of illegal funds through many small transactions that are below the legal reporting thresholds in a jurisdiction. The goal is to prevent attracting attention to the movement of the funds. Smurfing detection involves using AML transaction monitoring software to detect unusual patterns of transactions that could indicate smurfing.

Combating smurfing should be part of any effective Anti-Money Laundering compliance program. As well as robust transaction monitoring, strong Know Your Customer (KYC) and Customer Due Diligence (CDD) processes help to spot and stop attempts to create fake or compromised accounts used to facilitate the multiple transactions required for the technique.

FAQ

-

What are the 3 stages of money laundering?

Modern money laundering tends to be a multi-layered process with multiple stages that can overlap, repeat, or occur simultaneously. However, the traditional three stages of money laundering are placement (where illegal funds are introduced into the financial system), layering (where funds are separated from their source and placed into multiple “layered” transactions to make them harder to detect), and integration/extraction (where criminals receive the funds back in a way that appears legitimate). However, in practice, these stages often overlap and the boundaries between them can be blurred.

-

How does money laundering work?

Money laundering is the process of disguising illegally obtained money so it appears to come from legitimate sources. It typically involves three stages: placement (introducing illicit funds into the financial system), layering (moving the money through multiple transactions to obscure its origin), and integration (reintroducing the funds into the economy as seemingly legitimate money).

-

What is the difference between placement, layering, and integration?

Placement, layering, and integration are key elements of money laundering. Placement is where illegal funds are introduced into the financial system (e.g., by depositing cash into a bank). Layering is where the origin of the funds is obscured by putting them through multiple “layers” of transactions, often involving international transfers. Integration (also called ‘extraction’) is where the funds are returned to the criminals in a way that makes them appear to come from a legitimate source.

-

How can businesses detect and prevent money laundering?

Knowing how to prevent money laundering is essential for businesses, particularly those in the financial sector and other heavily regulated sectors. Regulated businesses must have robust AML processes in place to help them identify customers and assess their risk of money laundering, monitor customers' transactions for signs of suspicious activity, and swiftly investigate and report any such activity.

-

What are the penalties for money laundering?

The penalties for money laundering vary between jurisdictions but are generally very serious, including imprisonment, fines, and confiscation of assets. There are also serious penalties for regulated entities that do not comply with their Anti-Money Laundering (AML) obligations, including the potential for huge fines and restrictions on operating licenses.

Relevant articles

- Article

- Feb 3, 2026

- 11 min read

Arbitrage in Sports Betting & Gambling in 2026. Learn how iGaming businesses detect arbers using KYC & fraud prevention tools.

- Article

- Feb 16, 2026

- 9 min read

What is Sumsub anyway?

Not everyone loves compliance—but we do. Sumsub helps businesses verify users, prevent fraud, and meet regulatory requirements anywhere in the world, without compromises. From neobanks to mobility apps, we make sure honest users get in, and bad actors stay out.